Mistakes were made (I did a dumb thing)

Mistakes were made (I did a dumb thing)

“You can’t always get what you want. But you can try sometime and get what you need.” The Rolling Stones

Hi all.

The only things I can promise you in my writing are my curiosity, that I will be honest and vulnerable, and that I work hard to make the occasional paragraph flow nicely. If you’re interested in learning together about the business of life and investing, join me and 3,834 other subscribers.

“The speculator's chief enemies are always boring from within. It is inseparable from human nature to hope and to fear. In speculation when the market goes against you, you hope that every day will be the last day - and you lose more than you should had you not listened to hope - the same ally that is so potent a success-bringer to empire builders and pioneers, big and little.” Reminiscences of a Stock Operator

I like to write about my mistakes.

I don’t like making mistakes. But when I do, as frequently happens, I might as well share them. It has been liberating to stop pretending that I don’t get things wrong all the time. I hope it helps me learn and at the very least it clears my mental RAM. Better yet, maybe you find some entertainment in me stepping on yet another rake.

When I lost my job in 2020, I took it as a sign that I needed to get serious about figuring out a different path in my life. Unfortunately, locked up in my tiny New York apartment, facing a move back to Germany, and wrestling with anxiety about an uncertain future, I did the opposite of what I should have done. When markets were down and I should have invested, I held on to the safety of cash.

Whether it was growth stocks, value stocks, crypto, commodities, or real estate: at this point every asset class short of buggy whips seems to have had its moment in the sun. I felt envious of all the success I saw around me. I urgently wanted to rectify the divine injustice of being left behind. In other words: I was primed to make a greedy trade.

I found a pre-deal SPAC with a compelling VC sponsor and board. I felt there was a chance it could take a popular tech company public or find another target that would be well received in the wild market of early 2021. The downside was limited due to the cash redemption feature. I eagerly started pouring my money into this ticket to the good life, hoping to make up for lost time.

As the months passed and I got more information about the team and talked to other holders, my level of comfort and confidence increased. And I got more emotionally invested, firmly expecting a positive outcome. But wait: if I was so sure about this, the warrants would be an even better investment. They’d offer a chance at life-changing money. I started switching from an asymmetric and relatively liquid investment with low downside to warrants that trade by appointment. And I was giddy with anticipation.

Fast forward to fall 2021. After a period of strong issuance, and a string of bad deals, SPACs as an asset class fell out of favor. The premium valuations disappeared. The market became less enthusiastic about the upside and the warrants’ option value. Worse, the most interesting potential target for my SPAC raised another massive private round and was rumored to hire bankers for a traditional IPO. While there hadn’t been a bad deal, a good deal seemed less likely and timing more uncertain. My warrants rarely traded but when they did they dropped like a stone, from around $2 to $1 and change. The thesis wasn’t broken. But the price (and my brain) were.

Looking at my account triggered an accelerated grief cycle. This can’t be happening, I can’t believe this is happening, maybe I can fix it by sacrificing a goat, why does this always happen to me, and, oh my god, I fucked up again.

Facing an already tenuous writing career, I experienced visions of a future in which I told strangers about how I had gambled away my savings before retiring to the nearest tent city. I couldn’t think straight, struggled to fall asleep at night, and was not interested in waking up and facing the day.

Last year, uncertainty had led me to flee to safety. This year, trying to fix my past mistake led me to overtrade and take on way too much risk. I turned to friends for advice with the words: “Hey. I think I did a dumb thing. Again.”

Reset and regret

Stanley Druckenmiller, famous for “being a pig,” once recalled a lesson he learned from George Soros: “when you earn the right to be aggressive, you should be aggressive. The years that you start off with a large gain are the times that you should go for it. The way to build long-term returns is through preservation of capital and home runs. You can be far more aggressive when you’re making good profits.”

Notice that he said you had to earn the right to be aggressive. A friend of mine explained it to me as having a well-constructed baseline portfolio. Only with that steady state established can there be room for more risky and creative ideas. Plunging into my SPAC trade I had operated without room for retreat. I had burned the ships, then felt my coat catch fire.

In his speech at the Lost Tree Club, Druckenmiller recalled his trading record in 1999, when he had the “bright idea to short internet stocks” and quickly lost $600 million. He reconsidered, hired two young traders to trade tech stocks, and recovered the losses by going long.

By January 2000 however, he was convinced the boom was over:

“I’ll never forget it. I go into Soros’s office and say I’m selling all the tech stocks, selling everything. This is crazy. 104 times earnings. This is nuts. We’re going to step aside, wait for the next fat pitch.”

Once out of the market, he watched in frustration as the two youngsters kept making money. Eventually, he “couldn’t help himself.” He just “had to play.” He bought $6 billion worth of tech stocks. “I think I missed the top by an hour,” he reminisced. Six weeks later, he was out at Soros and the fund had lost $3 billion.

“You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself. Maybe I learned not to do it again, but I already knew that.”

Druckenmiller had re-learned a lesson about his HumanOS at the cost of billions of dollars.

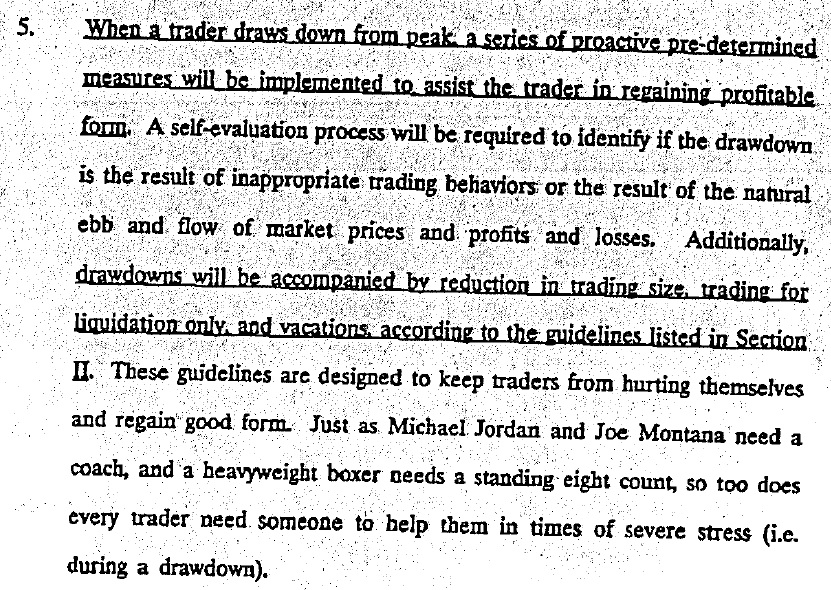

It is hard to think clearly in those moments, even for professionals. In a risk management memo from the 1990s, Paul Tudor Jones provided instructions on how to deal with an underperforming trader. Depending on the severity and length of the drawdown, the measures ranged from a short timeout away from the screen to closing out the book and sending the trader on forced multi-week getaways. The traders needed a complete reset and recovery from the pain and stress.

A friend commented on the pain of closing out a losing position: not only do you have to accept a painful mistake, you also have to let go of the chance of making it back. You have to accept the regret over missing out on future gains. That’s what I did. I hit the reset button.

Courtesy of another kind friend, I was able to spend a few days away from the everything. My first time at the beach this year. As I was meditating to the sound of the waves, I tried to let go of the last image I had seen before turning off my phone: the whole market was red, heading down on fears over the Evergrande default.

The whole market? No. Not the warrants. The warrants were trading up again.

My number one job is to ensure that I live to fight (and write) another day. But the idea of having puked my position at the bottom, out of fear and poor risk management, is almost unbearable. This has been a painful and expensive lesson about my HumanOS. Not the lesson I wanted, but perhaps the one I needed? Maybe I needed a final reminder that I am no Stanley Druckenmiller and never earned the right to make aggressive bets. But then again, I already knew that.

Enjoyed this piece? Let me know by hitting the ❤ like button.👇 Thank you!😉

wow this is brilliant, thank you for sharing your candid, thoughtful reflections! i speak only as a (wannabe) athlete, but sports and investing give us such harsh/effective life lessons. wishing you all the best, and come back stronger!