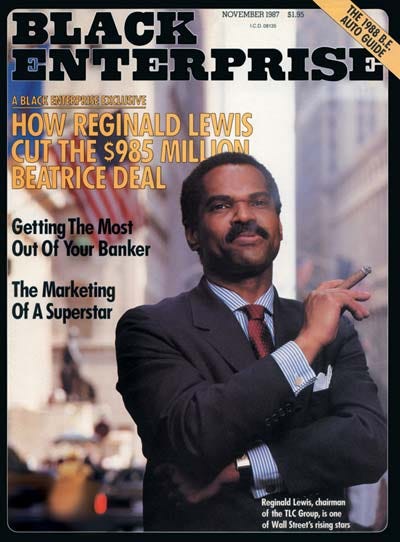

Reginald Lewis: Bootstrapping Buyouts

Reginald Lewis: Bootstrapping Buyouts

“People who get their thrills from talking about big deals end up not doing them. The fewer words, the better. It's action that counts, not words. That's the cardinal rule of deal-making.”

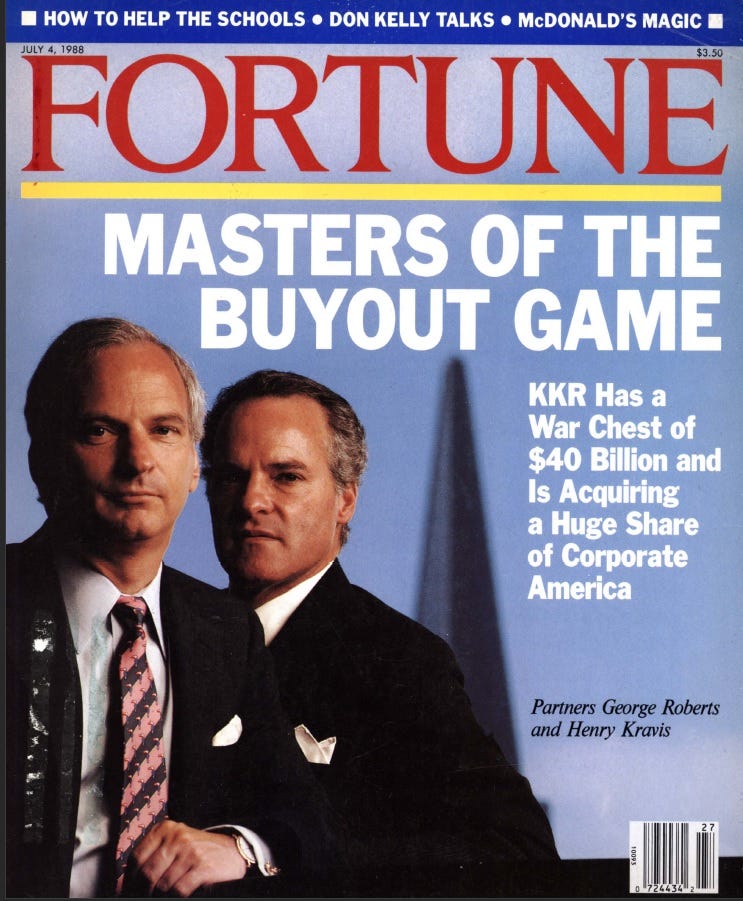

On Thanksgiving weekend 1987, an aspiring black dealmaker named Reginald Lewis walked into the offices of private equity firm KKR on 9 West 57th Street. In August, Lewis had won a $985 million bid to acquire the international food business of Beatrice, a conglomerate that KKR was dismantling. Then the stock market had crashed.

In a meeting with “King Henry” Kravis and bankers from Drexel Lewis asked for a price cut of $35 million. “If he doesn’t do it, I’m walking,” he had told his associates before the meeting. The December 1 closing deadline was fast approaching. Lewis and his team had been working around the clock. It was a deal that nobody thought he could pull off. If not for the personal backing of Michael Milken, KKR wouldn’t even have let Lewis bid in the first place.

Kravis was the last one to join the meeting. After hearing Lewis out, he said:

“We appreciate your views on the matter. We’ve done our analysis and we don’t quite get there the same way you do. We’ve really come a long way on this and we’d really like to see you consummate this deal. We’re pulling for you.”

There would be no price cut.

With all of his chips on the table, Lewis had to make a decision: walk away from the deal he had spent a lifetime preparing for, or channel the focus and determination that had gotten him this far. Fold his hand or “keep going no matter what,” as he often said.

“People who get their thrills from talking about big deals end up not doing them. The fewer words, the better. It's action that counts, not words. That's the cardinal rule of deal-making.”

“This is a success story due to the transaction, not because of my race. Iacocca is not cast as an Italian-American businessman and Icahn is not a Jewish-American. Why should I be an African-American?”

“Why the fuck do we have to prove ourselves over and over? I’ve got to go to the other side of the table. This is not the way I want to spend the rest of my life.”

“I was no overnight success. It took 25 years of hard work to get to where I am. That’s what everyone has missed.”

“I know I have cancer of the brain,” he told his wife, “I used my brain as a weapon to go forward and to disprove a lie about people of color, and I had no protection.”

Reginald Lewis

Reginald Lewis rose from a working-class neighborhood in Baltimore to become the first African-American to compete at the highest level in the game of corporate buyouts. His story is one of ambition, determination, fierce work ethic, and sacrifice.

After pulling all the stops to get into Harvard Law School, Lewis burned the midnight oil to build a successful law practice. Through his work he became familiar with the burgeoning private equity industry. Frustrated with the grind of being an advisor, he decided to put together his own deals. His crowning achievement was the $985 million buyout of Beatrice International in 1987. Only a few years later he tragically passed away from brain cancer. If not for his early death, I’m convinced he would be a household name today.

His biography “Why Should White Guys Have All the Fun” is a play-by-play account of his efforts to move to the other side of the table, to become an owner rather than an advisor. It shows how he bootstrapped his deals and doesn’t shy away from the personal sacrifice: Lewis dedicated much of his life to his work. His demanding and sometimes brash nature led to falling-outs with partners and associates. It’s a great book if you’re putting together deals yourself, particularly if you’re looking for inspiration after a setback. Lewis faced long odds and a steep learning curve: some of his early deals fell through at the last minute, prompting him to question everything.

What impressed me most were his focus and determination. Once Lewis had his mind set on a goal, no matter how unlikely it seemed to others, he wouldn’t stop fighting for it. He worked day and night until he broke through whatever wall separated him from success.

Lewis was born in 1946 and grew up in Baltimore with his mother and grandparents.

“My mother left my father when I was 5 and arrived at grandma’s house in the middle of the night with me under her arm.”

His mother told his grandparents that she and her young son would not be a burden and pay their share in the household. Lewis rarely saw her as a boy: she worked two jobs, as a waitress and department store clerk. “That stuck,” he said. From a young age, he was hardworking and ambitious.

Throughout his schoolyears he worked a variety of jobs, starting with paper routes and ending with a summer as a waiter at the country club where his grandfather worked. His grandfather told him: “always remember, your skill is what’s important. Get that and build on it and sooner or later you’ll have a big payday—count on it.” Years later, Lewis would take him for lunch at the Harvard Club. Lewis told a friend it had been one of his life’s proudest moments.

At first it looked like football was going to be his ticket to a good life: he attended Virginia State University on a football scholarship. But a shoulder injury squashed that dream. Lewis had been working a variety of jobs, including arranging student yearbook photographs and night shifts at a bowling alley. As a result, his grades had suffered. All of a sudden he found himself disoriented and without a clear path forward.

Never take “no” for an answer: getting into Harvard

I grew up in a small German town where rules and order were important and followed to a tee. Even with no cars in sight, people stood at the red light, refusing to cross the street. It took some time in New York before I lost that habit. As a result, I’m fascinated by people who refuse to accept the rules, who don’t accept the limitations separating them from their dreams.

This was Lewis, when he heard about an initiative by Harvard Law School. A new two-month summer program introduced minority students to the field of legal studies. It was designed for college juniors who could then prepare to apply for law school. Colleges could submit a shortlist of suggested candidates for Harvard’s consideration.

Lewis was already a senior. And with his mediocre grades he wasn’t on his school’s shortlist. And yet, he ended up going.

Once he realized the potential of the situation, he became laser focused on this goal: figure out a way into the program. Then turn it into an admission to law school, even though that was explicitly not the purpose of the program.

“An incredible calm came over me and the plan began to emerge. First, have a tremendous final year in college; second, know the objectives of the program; third, break your ass over the summer, eliminate all distractions—nothing except the objective.”

“It wasn’t easy knowing where to begin. First, I needed to get the literature on the program. My school only gave a summary of it, so I wrote to Harvard for specific details the same day I found out about the program. Harvard responded immediately, which really impressed me.”

First, he read everything he could find about the program. Then he worked with his favorite professor to obtain an extensive and enthusiastic recommendation letter. His school agreed to add Lewis to the initial list. And with the letter standing out, Harvard selected him for the program.

Lewis mapped out the next stage of his plan:

“During the first semester, say nothing about going to Harvard. First, prove that you can compete; for example, take a difficult course at Harvard College during the summer and do well. Second, do the job. Build upon your strengths. This was the brief and I’ve never executed better.”

The program ended with a mock trial for which Lewis had prepared extensively. He brought all his energy and focus to the table and was rated among the best students for the course. He had bonded with the professor running the program and sought him out after the trial. Now there was no more downside to asking about admission. This was the program’s first run and he was perhaps the first and only student who had a chance at turning it into an admission ticket.

Over the course of the summer he had cultivated several other professors who were impressed by his interest and work ethic. They became his advocates with the vice dean whose decision it was. Incredibly, Lewis convinced the school to admit him based on his performance (academically and socially) during the program.

“I’m told that I am the only person in the 148-year-history of Harvard Law who was ever admitted before he applied.”

I’m not suggesting the same could be accomplished today. The lesson to me was that Lewis saw a unique opportunity in front of him. This path was not possible according to the rules set out by the program. Lewis’s goal was behind barbed wire. He was in the wrong school year, had mediocre grades, and nobody was supposed to be admitted from the program to law school anyway. However, his instinct told him it could be done. He invested all of his time and energy into trying and succeeded in lifting himself on an entirely new track in life.

Lewis graduated from Harvard Law School as a member of the class of 1968. Shortly before his death in 1992, he made a $3 million gift to establish the Reginald F. Lewis International Law Center, the first building on campus named after an African-American.

Grinding it out

Despite graduating from one of the country’s best schools, Lewis’s time as a lawyer was anything but easy. He had a promising start, joining the prestigious law firm Paul Weiss as an associate. But he heard that he wouldn’t be on track to make partner and decided to leave after only two years. He joined a group of lawyers to form a new firm: Murphy, Thorpe & Lewis. While the other partners left, one after another, over the course of several years, Lewis carried on, grinding all week to find clients and occasionally dipping into his savings to make payroll.

“I was already working about 12 hours a day and for the next year I must have kicked it up to about 18 hours a day during the week and 6 to 8 hours on Saturdays and Sundays.”

His biography makes it clear that he was tough to work for: highly demanding, brash, hard-charging.

“Everybody was afraid of Reg over the years and it got worse,” Clarkson says. “He would treat the opposition with kid gloves and he would scream at everybody else on his side of the table. It was warfare all the time with Reg.”

Eventually he found a profitable niche: a newly established government program called MESBIC which provided capital for minority-owned businesses (today the SBA still provides government-backed loans to smaller businesses). Through his work he developed a network of entrepreneurs and bankers and cut his teeth on the structuring of acquisitions and buyouts.

Becoming the client

“I've spent a lot of time representing acquirers. I know how to get transactions done. Plus, I want to do something that will allow me to make money while I'm sleeping.”

As an advisor, Lewis helped his clients execute deal after deal and, presumably, quickly noticed the discrepancy between his own grind for billable hours and the rapid and scalable wealth creation possible through good investment decisions.

The size of his business was determined by his own billable hours, his price per hour, and his ability to grow the firm with more partners and associates. All of these factors faced real constraints, including his own temperament and willingness to share control of the firm. Meanwhile, deals offered scale through the use of other people’s money, from bank debt to junk bonds and junior debt and equity offered through the MESBIC network. Naturally, he decided to put together deals of his own.

Or in his words:

“Why the fuck do we have to prove ourselves over and over? I’ve got to go to the other side of the table. This is not the way I want to spend the rest of my life.”

He started talking to brokers, looking for “low-tech, high cash flow, and good management” businesses. His early attempts included a sausage company in his hometown Baltimore and a manufacturer of beach chairs.

The deals got close to but not across the finish line. Parks Sausage was sold to a group that showed up later in the process but carried more credibility and capital. The seller of the beach chair company backed out at the last moment, then sold the company later for a higher price. Unsurprisingly, Lewis was frustrated.

“When something like that happens to you and when you are inexperienced and let your ego run wild, you are crushed. You second-guess every decision you made, when rarely does any of that matter.”

“The only conclusion I could reach was that even after finding the needle in the haystack, putting together great financing, courting a 61-year-old businessman, getting a definitive contract signed without a penny up front and more, much more, I STILL WAS NOT READY.”

These deals became important lessons. Lewis realized that he couldn’t run point on all aspects of a deal, let alone also manage a law firm at the same time. He became more thoughtful about assembling a team of advisors. He also recognized the importance of incentives: for the advisors involved and for the management team controlling the asset.

“The hardest fact to come to grips with was that many of your strengths can indeed be weaknesses at different stages in the deal process. For example, in Almet, I was the finder of the deal, chief financial analyst, fundraiser, quasi-legal officer, and chief strategist. In short, I was going about it assbackwards. For five years, I had gone about it all wrong, using an approach that could get me close, but not get the job done. A hard pill to swallow.”

“Another issue which emerged quite quickly was to take the emotion out of the equation to the fullest extent possible. These were business transactions, nothing more. Not jousts, tests of moral fiber, etc. Of course, passion is often important to get a project started, but once it gets going, the pendulum shifts very quickly to cold calculation from passion.”

“Most of the people who were good at this were involved full time. Part-time deal-making is almost a contradiction in terms. Also, forget about the old boy network. What was driving transactions in today’s market was fees. Fees to the banks, the investment bankers, the lawyers, the accountants, the deal-finders. Strong economic incentives were very much the order of the day.”

Building a winning process

Perhaps the most important insight was that he needed to improve his sourcing effort. He started to follow a disciplined process of calling up his network of bankers to constantly ask for more “product” (ideas in the form of transaction prospectuses). And he had to dedicate the time to read and process all that information to find the right opportunities.

“I then became a prospectus junkie and read all the deals which were publicly reported. It is amazing how much you can learn from public records about how people go about things.”

He channeled a different aspect of his personality: rather than hustling to find clients, he imitated Warren Buffett. He had to sit and read document after document, until the network of data points started to surface actionable ideas.

From his biography:

“Most people would have found the prospectuses incredibly tedious reading, but not Lewis. He read them closely, dreaming a little and learning a lot. Each prospectus was like a little history book that told Lewis about the officers of a company, their salaries, their strategic thinking—even about lawsuits filed against a company. Lewis ate all of this up and he liked nothing better than to take a set of prospectuses home to read.”

McCall Pattern: Deep Value Private Equity

The stars aligned for Lewis in 1983, when he read an article about the merger of two conglomerates: Esmark and Norton Simon. Esmark’s CEO had mentioned several business units he wasn’t interested in, including one called McCall Pattern.

McCall was the second largest player in the shrinking market of home sewing patterns: paper cutouts used to sew clothing such as dresses or skirts. Incredibly, this business is still around today. However, in the 1980’s the industry was in decline already and Lewis correctly concluded that the company wouldn’t attract much attention or competing bidders.

“A lot of people had written off [McCall] as not having much of a future, [but] the more I researched the facts the more I thought it had a great future, because its strongest asset was its most fundamental asset of all, and that was the people. It had a wonderful group of employees at the top, the middle and throughout the organization who had excellent experience, who knew their business very well and who were committed to doing what was necessary to keep the company dynamic. The company had actually performed very well for a long period of time. When I delved into the facts, I decided that the fundamentals were actually quite good.”

Lewis saw a leading business, albeit in a shrinking market, with attractive margins and strong cash generation. If he could buy the company at a very low valuation and improve the cash flow, he could pay down debt and sell the business a few years later. It was private equity 101 with a deep value asset.

Finally, Lewis could apply the lessons of his failed deals:

He had set up his own buyout firm, called TLC or The Lewis Company, and had a dedicated team to support him. Bear Stearns was working for him to arrange bank financing. Lewis could focus entirely on building the relationship with the seller and the management team, negotiating terms, and managing the overall deal process.

After building rapport with executives at the parent company, he charmed the McCall management team. He learned they had tried to structure their own management buyout and realized that equity upside would be important. He took Earle Angstadt, McCall’s President, for lunch to the Harvard Club. When asked “what are you going to do for management,” he was prepared to offer equity and a chance for significantly upside. Angstadt became his ally and lobbied internally on Lewis’s behalf.

“He had all of his thoughts and proposals well organized. We related to each other very quickly in our first meeting. My first instinct was that this was the man with whom I wanted to make a deal.” Earle Angstadt

Instead of presenting himself as a sole bidder, he said he acted on behalf of a “group of investors.” The group consisted primarily of Lewis and two friends who contributed $10,000 and $5,000 respectively. Still, it was a group. Lewis reasoned that his counterparts would automatically assume the investors behind the group were white. The undisclosed group provided a way to eliminate the risk of losing the deal due to racial prejudice, a factor he suspected had played into one of the failed deals.

Lewis saw the parent company had pulled $18 million of cash out of the business over the prior 2.5 years. That was his initial lowball bid: $18 million for a company with $6 million in operating profit. In order to win the deal he ended up raising his bid to $22.5 million: $20 million cash and $2.5 million of seller notes.

“McCall was earning about $6 million in operating profit. This was a figure I would repeat often. The fact is, however, I never focused on earnings. Others like to hear it so I repeated it, but I kept my eyes glued on cash flow. When I worked through the numbers, over a 2½-year period NSI had pulled about $18 million in cash out of McCall. That, then, was my price—$18 million. In my heart I was ready to go higher.”

When his bankers were slow to arrange the financing, he called up their competitors at Drexel. This created a competitive dynamic and opened the door for future conversations with Michael Milken.

The final deal was an impressive example of bootstrapping: Bankers Trust provided $19 million of senior bank debt. An MESBIC lender provided $0.5 million of junior capital. $2.5 million in seller notes were owed to Esmark. Management put in $0.2 million of cash. Lewis himself borrowed $0.5 million from his bank to contribute as cash equity. He acquired control of a company valued at $22.5 million with only $0.5 million in borrowed cash.

After the closing dinner he told an exhausted partner: “You don’t have to come in tomorrow, take Saturday off. Just come ready to deal on Monday.”

Rolling up the sleeves

With his eye on boosting cash flows, Lewis made some key changes to McCall:

To boost working capital, bills were paid within 30 days rather than immediately.

Lewis had the idea of using idle time on the printing presses to make greeting cards which turned into an additional profitable business line.

The remaining sewing pattern companies regularly fought over market share. When McCall’s largest competitor offered promotional discounts, McCall’s management followed suit. This cost the company $2 million. Lewis was furious and ordered that the company would no longer offer discounts. He was willing to lose market share in favor of maintaining price discipline.

He pushed the management team to set aggressive targets for the year and offered significant bonuses. Management earned maximum bonuses every year under Lewis.

Lastly, he turned the company’s real estate into cash. His private equity firm acquired the warehouse property and leased it back to the company.

With fresh liquidity and increasing cash flows, Lewis refinanced the debt and distributed cash to shareholders.

McCall’s operating income increased from $6 million in 1983 to $12 million in 1985 and $14 million in 1986. But it was still a business in a declining industry and Lewis had no interest in owning it for the long term. With much improved cash flow, it was ready to be sold.

In 1987, Lewis sold McCall to a British textile company for $65 million plus assumption of the debt. The return on his equity investment was astronomical. Shareholders received $65 million plus dividends and gains on the real estate. He counted around $90 million in value compared to an equity investment of around $1 million. A ninety-bagger in a few short years. That number would become very important to Lewis.

The value of a reputation

Lewis instinctively understood the importance of his reputation in the financial community. Sellers had to trust him to close the deal. Lenders were worried about being paid back. Equity partners wanted someone with a track record of strong returns.

Shortly after selling McCall, he noticed an article that he felt omitted his role in improving the business. He called the reporter to voice his frustration. Needless to say, the reporter didn’t appreciate being yelled at. After the call, Lewis recognized his mistake: the media could be his ally if he found a way to better manage the relationship.

He immediately hired an experienced PR firm whose representative arranged an interview with the reporter. The effort was a success, with the New York Times publishing a highly flattering article titled: “90-1 Return for Investor.” Lewis and his team would send copies of this article to anyone they dealt with.

From the article:

Reginald F. Lewis's first leveraged buyout was for a relatively small company, but it was a huge success. He cashed out with a 90 - to – 1 return. Mr. Lewis and his investors put up $1 million in equity and received $90 million on that investment in three years.

''This kind of return puts you in the top, top, upper levels,'' said Maynard Toll, an investment banker at the First Boston Corporation who has worked with Mr. Lewis. ''He is a very creative financial person.”

''Unlike some financial people, Mr. Lewis rolled up his sleeves and got involved in the direction of his company,'' Mr. Toll said.

Mr. Lewis, 44, is an intense lawyer who is likely to call an associate at 6 A.M. to deal with a problem.

A few years later, McCall ran into trouble and Lewis was sued by the new owner and bank lender. For Lewis, more than money was at stake. The lawsuit threatened a cornerstone of his reputation. He refused to settle and fought for years in court. Eventually, he prevailed.

As one of his partners said: “We were at war—that was the mindset. It was one of the toughest periods during my 12-plus years with him. He would react with more vehemence on issues in the litigation than on almost anything else I can remember.”

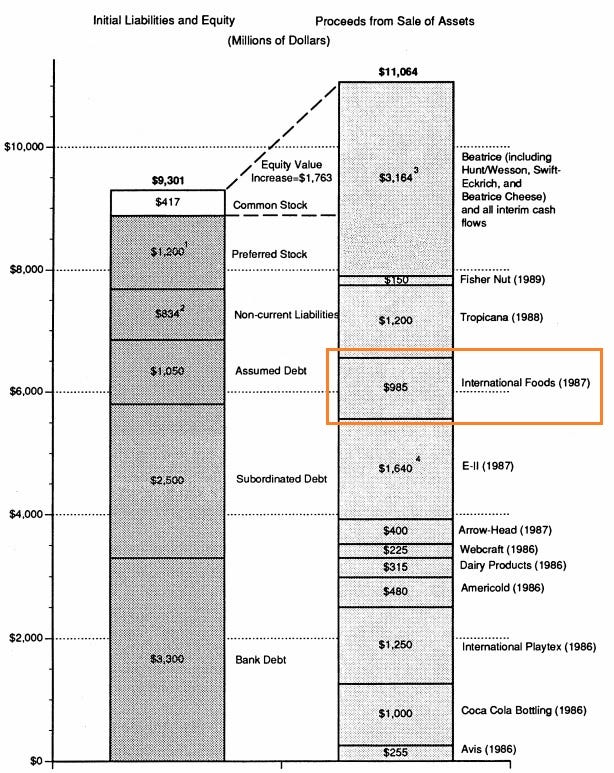

Beatrice: carving up a conglomerate

Beatrice was founded in 1891 as a small creamery. Through acquisitions it turned into a sprawling food conglomerate.

From the paper: “Beatrice: A Study in the Creation and Destruction of Value”

“Widely admired as one of America's best run companies in the early 1970s, the firm struggled with problems of strategic direction and internal governance in the late 1970s, which resulted in tremendous value loss. In large part because of this value destruction, Beatrice was caught up in the financial restructuring mechanisms of the 1980s and was taken over in a LBO in 1986 that led to the sale of all the assets of the firm within four years.”

The FTC had barred Beatrice from further acquisitions of dairy businesses. As a result, the company had started to diversify into other food and even non-food operations. In its final stretch of dealmaking, Beatrice’s CEO bid for another conglomerate, Esmark, which itself had just acquired the conglomerate Norton Simon (and sold McCall to Lewis).

While Beatrice bid for Esmark, Esmark’s CEO Don Kelly had partnered with KKR to take Esmark private. However, Beatrice outbid them and acquired the company. The former dairy company now owned brands such as Tropicana and Playtex, Coca Cola bottling plants, and even Avis Car Rental.

In a hilarious twist, Kelly then partnered with KKR to acquire Beatrice. It was an $8 billion deal and the largest buyout at the time. After the deal closed, Kelly and KKR started selling off the various business units.

Beatrice: acquisitions followed by divestitures:

Growth of Beatrice’s assets:

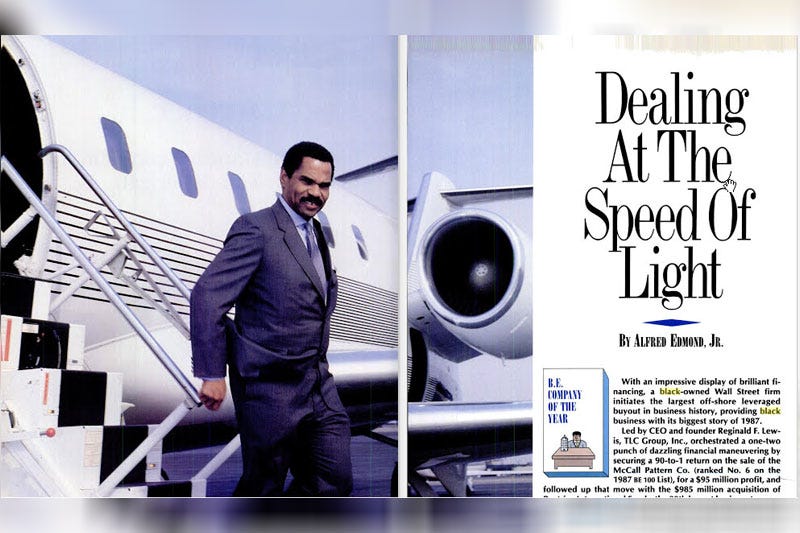

Dealing at the speed of light

The ink on the McCall documents was barely dry when Lewis got a call from one of his bankers. KKR was selling Beatrice’s international foods unit. Lewis was exhausted and nearly declined to read the prospectus, but the banker insisted: “this thing has business and assets all over the place. You’ve told us of your strong desire to go international and your desire to be diverse.”

Beatrice International, one of the many assets being sold from Beatrice:

Beatrice International was in many ways the opposite of McCall Pattern: it was a good and growing business (branded consumer goods and some grocery retail in France), it was complex and global (64 subsidiaries in 31 countries, often with local partners as minority owners), and it was significantly larger with $2.5 billion in sales and $145 million operating income. Lewis still had no fund, just his own capital and whatever leverage the market would provide.

It was also a well-publicized and highly competitive deal. The bankers received dozens of initial bids from private equity groups and large food companies such as Pillsbury. Lewis read the prospectus and collected his thoughts:

“What’s interesting about this company and what isn’t? How would I manage it? Who’s the competition? What price will this thing fetch? What is the quality of management? Are there hidden assets? I decided to list all the things I did not like about the situation and then see if those “dislikes” could actually be disguised benefits.”

His associate built a financial model overnight and Lewis ordered his banker back from her vacation on Cape Cod the same day. Days later he submitted a bid for $950 million.

Lewis received a call from the bankers running the sale: “We have received from your group an offer to buy Beatrice International for $950 million. We have a small problem—nobody knows who the hell you are!”

Despite his success with McCall, he was still an unknown quantity. But he had cultivated a secret weapon: Michael Milken. Since buying McCall, he had stayed in touch with people at Drexel and eventually met Milken in person. Confident in Lewis’s ability, Milken backed him in the Beatrice transaction.

Lewis laid out his plan:

“Michael, yesterday we bid $950 million to KKR for Beatrice International Foods. Beatrice International has $2.5 billion in sales, $145 million of operating income, and 64 companies in 31 countries. Our plan is simple: Bid the whole thing and simultaneously, with our acquisition, we sell Canada for $200 million, we sell Australia for $75 million, we sell Latin America, maybe for $100 million. So now we’ve pared away about $400 million, and we’ve still got a company with $2 billion in sales and over $100 million of operating capital. But now we’ve only paid $550 million to $600 million.”

On a visit to KKR, Milken met Henry Kravis who said: “Michael, on this Reg Lewis – I know he’s made a lot of money on the McCall deal, but he has no credibility with me on a billion-dollar deal.”

Milken responded: “Well Henry, he’s got credibility with me.”

And with that, Lewis was in the game.

Michael Milken, Loida Lewis (Reginald Lewis’s wife) and Reginald Lewis:

Pulling off the impossible deal

On August 6, 1987, Lewis signed the agreement to acquire Beatrice International. He had until December 1 to close the deal.

“He would come into his 99 Wall Street office around 8:30 A.M. and work on things related to the Beatrice bid until around 3 in the morning. On the weekends he took something of a break, getting into his office around 9 A.M. and leaving around 11 P.M.”

Lewis and his team worked around the clock in their due diligence and negotiations. The deal was structured such that several international businesses were sold off to local buyers at closing, leaving Lewis with a more focused, primarily European, collection of assets (and less leverage as the business units were sold at higher valuations). Many remaining businesses had local partners. Lewis had access to one of Beatrice’s corporate jets and soon travelled around Europe to visit facilities and negotiate with the local partners.

The international subsidiaries presented a significant hurdle to a highly leveraged deal: income was generated and taxed locally, before the cash was sent to the parent company where it would service the debt. This meant that the interest expense at the parent didn’t shield the income from taxes, a key feature of leverage buyouts.

Lewis’s associate Christophe:

"We developed the best strategy for acquiring a firm with all of its operating income outside the United States, with financing from the world's most efficient capital markets, which were in the United States. One needed to do that in order to maximize the interest deductibility from a taxation standpoint. We figured that out better than anyone else."

With his legal training and tenacity, Lewis was better suited than most to deal with this problem. Not for nothing did he donate to Harvard to create the Reginal Lewis International Law Center. Eventually he decided to set up a French holding company that became a borrower and could deduct interest for tax purposes. The structure required approval from the French ministry of finance, which Lewis personally negotiated with the ministry’s first deputy.

“There could not have been any greater pressure in any deal Reg ever did,” Tom Lamia said of the French negotiations. “I think it was only when he got French government approval that he saw that the Beatrice deal was going to be done.”

In exchange for being kingmaker, Drexel also demanded its pound of flesh in the form of equity. At one point, the Drexel bankers even asked for a controlling stake. Lewis threatened to blow up the entire deal and Milken had to intervene. Drexel ended up with around a third of the equity.

Keep going, no matter what

After the October stock market crash, Lewis tried in vain to negotiate a lower price with KKR. Henry Kravis understood that Lewis was deeply committed to the deal. This this was the opportunity of a lifetime for the up-and-coming dealmaker.

Sure, public valuations had declined. But Drexel was still arranging most of the capital in the form of debt. After selling the Canadian, Australian, and Asian operations for $430 million, Lewis would acquire control of the remaining company almost entirely with debt. He contributed only $15 million of his own cash equity to gain control. Drexel and management would own a combined minority share of 45%.

Lewis kept going and closed the deal on November 30, 1987.

The closing was an enormous and grueling two day affair: it involved 180 lawyers, accountants, financial advisors, and executives. Teams were spread out over six floors at Lewis’s old law firm Paul Weiss. It was really a series of mini closings of acquisitions, sales, syndicated bank debt, and subordinated debt. Investment banking and legal fees amounted to $54 million.

Within six months Lewis sold the Latin American business to further cut the debt load. By personally acquiring equity in the business unit prior to the sale, he also recouped most of his equity investment. Not only did he control Beatrice International (now TLC Beatrice), he was effectively playing with house money.

Thanks to a weaker U.S. dollar and streamlined operations, TLC Beatrice grew its operating profits more than 50% from 1988 to 1990.

“We earned $1.5 billion in sales, close to $100 million in operating income, and $45 million after taxes. So on a buyout, we earned $3.62 a share on our common stock. You have to remember that the common stock had cost $1.”

Lewis had only a few years to enjoy his success. He tragically died of brain cancer in 1992. His widow eventually took charge of the company, steadied it, then proceeded to sell off business units throughout the late 1990’s. Shareholders reportedly received distributions of hundreds of millions of dollars.

“I know I have cancer of the brain,” he told his wife, “I used my brain as a weapon to go forward and to disprove a lie about people of color, and I had no protection.”

The above picture is from Fortune Magazine. Unsurprisingly, Lewis’s successful “billion dollar buyout” (though effectively smaller because he de-risked the transaction by selling pieces off at the same time) attracted a lot of media coverage. All of a sudden, Lewis was the “first black man to lead a company with a billion dollars in sales.”

Lewis was frustrated by the focus on his race rather than his business and legal acumen. When he felt that a reporter was too focused on that angle of the story, he stopped calling them back.

From the LA Times:

“It's understandable that [my race] is something people focus on. But what I focus on are two different things. I focus on doing a first-rate job on a consistent basis.”

He rejected the narrative that his success, or his downfall if the highly leveraged deal were to go wrong, had greater symbolic significance. He always nudged the focus back to the merits of the transactions and the businesses he was involved with.

“To carry around the notion that if I fail, it's going to mean that no other black person will ever have a similar opportunity, or that if I succeed, it's going to open a floodgate of opportunity for other black Americans, misses the point," he said at the time. "If our work is perceived as an indication that we can function in a global, competitive situation, that's nice. But I've always believed that anyway.”

“I’m not going to carry my race on my shoulder,” he once told a close confidante. “If I can be helpful to others, that’s fine, but I’m not going to do my work because I am a role model for all African-Americans. That’s bunk. I’m not responsible for anybody’s life, I’m responsible for my life. And I’m responsible for realizing my own dreams.”

That doesn’t mean he forgot the hurdles and prejudice he experienced throughout his life.

“Every African-American male who’s worth anything has a sense of anger built up in him against society.”

I found his story both incredibly inspirational and tragic. He achieved so much through sheer force of will, and had such little time to enjoy his triumph. And even though he loathed the focus on his background, there is no doubt that his success motivated many. Kenneth Frazier, CEO of Merck:

“Reg Lewis opened up a world of possibilities for an entire generation of black business leaders. I distinctly recall my reaction when he engineered the acquisition of Beatrice Foods. I said to myself, “Who is this brother?’”

Despite all hurdles and setbacks, Lewis kept going, kept chasing his dreams and carving his own path. I highly recommend his biography and the documentaries about him (see links below).

That’s it for this week. I hope you enjoyed it!

“Even in my own career, a person of very modest means has been able—by dint of his own efforts—to achieve great wealth and financial independence, which therefore suggests that some progress clearly has been made. But in my view, it is all too little when we consider the day-to-day drama being inflicted upon many of our children who are of African or Hispanic descent and who are not yet fully included in the American Dream. Hard work, discipline, being focused, and having your skill knitted together in terms of what’s needed to get the job done.”

More on Lewis:

Documentary: Pioneers: Reginald F. Lewis (with snippets of Jesse Jackson, Milken, Kravis, Ken Chenault)

Documentary: The Reginald F. Lewis Story

Biography: Why Should White Guys Have All the Fun?

NYT Obituary

Nice Writing. Enjoyed reading it. I will definitely read his auto-biography. I looked for him after reading about him on Dr Strive Masiyiwa's page.

excellent read!!!