Yes Before No: How Dan Gilbert Conquered Mortgage Lending (#1)

Yes Before No: How Dan Gilbert Conquered Mortgage Lending (#1)

What I learned about the history, success, and culture of Rocket Companies

I’m fascinated when I come across a company that succeeded in a boring old industry by slowly and steadily building a better mousetrap. Rocket Companies fits this mold, conquering the mortgage market with a unique culture, incremental innovations, and relentless execution. It is a fascinating story that starts with Dan Gilbert as a part-time real estate broker and ends with the IPO of America’s largest mortgage lender.

In this piece I will first walk through the history of Dan Gilbert and his company, then take a look at some of the drivers behind their success. Finally, I will discuss the collection of principles or “Isms” that anchor the company’s culture.

A quick note on names: the company was first called Rock Financial before becoming Quicken Loans. Quicken Loans is now a subsidiary of the Rocket Companies (the publicly traded company) which is a part of Gilbert’s “Rock family of companies” and runs Rocket Mortgage - the digital mortgage platform. Got it? 😊

Quotes are by Dan Gilbert unless otherwise noted.

Disclaimer: this is not investment advice and not an opinion on Rocket Companies or the company’s securities. As such, I will not comment on the offering, valuation, or financials. Always do your own work.

©Rocket Companies

Ready to Rock: The Story of Dan Gilbert

"There was no grand thesis. It was just sort of go in there and hustle for a little bit."

Dan had an early start as an entrepreneur. First, he sold candy to classmates, then he came up with a pizza delivery business at age 12. He baked the pizzas in his mom’s kitchen and recruited his younger brother Gary and friends for bike delivery. This venture was eventually shut down by the health department.

"Some local pizza joint must have tipped off the health department. It was my first exposure to regulations."

As an undergrad at Michigan State, Gilbert ran a football betting ring with friends. As the story goes, a kid who "couldn't cover his debts" called his father for help. The father got the police involved who sent in an undercover cop wearing a wire posing as a dad. Gilbert ended up with 100 hours of community service. According to the prosecutor "it was a pretty sophisticated operation, way above average for what I knew of so-called organized crime.”

Gilbert’s parents wanted him to be a lawyer and so he enrolled at Wayne State Law School. His parents also had a Century 21 real estate brokerage where he started working part-time. To attract customers, he put a "for sale" sign on his parents' lawn (the house was not for sale). He would then show other homes to the prospects attracted by the sign.

"I don't know why I went to law school. I don't even know where my diploma is today."

Gilbert realized that he could make more money brokering mortgages. It was neither a glamorous start nor driven by a big vision.

"I landed on mortgages through selling real estate part time, learning a little bit at a time. We were 23, and we barely knew what a mortgage was.”

Together with his brother and two friends he started Rock Financial Mortgage in a shared office space with and $5,000. They called it "Rock" because "it sounded solid."

“I went into one of those shared office suites in the summer of 1985. Beige and grey and ugly. Across the hall was a lie detector guy.”

At the time, mortgage brokers typically relied on relationships with realtors for leads. But Gilbert was an outsider and didn’t care about the industry’s conventions. So what if others didn’t advertise home loans. He asked his team: "why are we going through a middleman, the realtors, to get to the customer? Why not get to the clients first?” For example, the team bought cheap ad space in free real estate newspapers, a marketing channel considered somewhat sketchy by established lenders.

"From the very beginning we could make the phones ring even if we didn't know what to do once they rang."

Building a Better Process

“Mortgage lending in this country has always been localized and it’s fragmented. We made a commitment. We’re gonna put a bunch of people in a room and get licensed in all 50 states. And we’re gonna figure out how 3,000 counties close loans across the United States. And do it centralized, with technology. It’s not about money or capital, it’s not even about brains, it’s about time. It’s about [being] willing to go through the process, the hell, of going through this stuff.”

Gilbert realized how slow and cumbersome the mortgage process was for borrowers and started to think about ways to streamline the experience. He called the mortgage business "the worst in the world."

"Only 11% of mortgage customers say they'd recommend their lender to a friend."

Looking for new ideas, he thought about the 1-800 CONTACTS business model. If he had a centralized call center, he could break down the underwriting process into steps and distribute the work among teams of specialists. This would allow him to optimize the process compared to having a team of local loan officers managing the entire transaction. Loan officers in the call center would be assigned to specific regions, becoming familiar with the local regulations and nuances.

The company opened its first call center in 1996. It developed the "Mortgage-In-A-Box" - a loan application that could be filled out at home rather than at a bank or broker’s office.

Picture via Kosta Baltzoglou

"We recognized early on that whoever's the most efficient through technology is going to have a lower cost structure. The company is far from the model of a traditional mortgage lender. We try to run it with as little bureaucracy as possible and let the (employees) have a say."

In 1998, Gilbert took Rock Financial public. That same year he also recognized the importance of the internet. The company launched rockloans.com to offer mortgages online.

With the benefit of hindsight this may seem like a nobrainer. However, as Gilbert explains, at the time there was still significant doubt whether major transactions would be done online.

“We did surveys with our clients. What percentage of you would put your financial information into a computer. 96% said they’d never do it. So we closed all the branches and started it anyway.”

He started closing branch offices and commented on the gains in efficiency:

"A good loan processor of ours used to get 50 or 55 loans to the table every month, but now a good one can get over 125, because the paperwork has been reduced so much.”

Quicken

At the height of the dot-com bubble in 1999, Rock Financial was acquired by Intuit for $532 million. Intuit, the company behind TurboTax and Quicken software, wanted to offer financial products to its 25 million customers. It had already started its own QuickenLoans offering, including a QuickenMortgage website where visitors could compare loans from different lenders.

However, Intuit’s approach of generating leads for mortgage lenders had a major issue: it wasn’t converting. Too few prospects ended up closing a loan.

Gilbert had a strong opinion on this approach:

“Multilender sites are not profitable. They don’t work. They never will.”

As a result, Intuit talked to a dozen companies and decided to acquire Rock Financial. Countrywide commented: "That's what drove Quicken to make the purchase of Rock. There's a recognition that when people are online, they want to apply immediately-make it happen as quickly as possible. Quicken needed to close the loop in the transaction."

Gilbert’s emphasis on streamlining and speeding up the process was exactly what Intuit had been looking for.

However, integrating the fast-moving Rock Financial into Intuit proved difficult. In a throwback to the days when software was shipped on CDs, Gilbert was told his offering would on the “2004/5 version.”

“That’s a century for me to wait, that’s like a lifetime.”

In 2002, Gilbert turned 40 and decided to step down and retire. To his surprise, Intuit’s CEO flew to Detroit to attend the goodbye party. Afterwards, he offered Gilbert to buy back the company. Intuit wanted to focus on software exclusively. Gilbert agreed and repurchased the mortgage business, together with a license for the Quicken name, for just $64 million.

Since then, the company has continued to focus on streamlining and automating the mortgage process. This culminated in the launch of Rocket Mortgage in 2015, the first fully digital mortgage platform.

"We tie into payroll services and IRS for verification, into every bank in the country for assets, into appraisal databases to get values, into credit bureaus. Within eight minutes - we say it's eight minutes because all the focus groups wouldn't believe it's one or two minutes, which it is."

It seems the company also weathered the mortgage crisis fairly well, although I found surprisingly little detail about that time. There was a wave of layoffs and the decision was made to exit any nonconforming mortgage business (loans not accepted by Fannie Mae or Freddie Mac). As one executive said:

"It was the first Tuesday in August that all hell broke loose. Dan sent an e-mail: 'Get a war room set up overnight and we'll be in here first thing tomorrow morning.'"

Quicken Vice Chairman Bill Emerson said that executives had stayed in the war room 18 hours a day for 8 weeks to fix the business:

"We turned this thing around in a week and went from some of the stuff that we were originating to a 100 percent Fannie-Freddie shop."

Notably, the company entered mortgage servicing in 2010, a time when the industry was decimated.

Quicken was also later accused of making errors in its pre-crisis underwriting. Gilbert refused to settle and the case was dismissed in 2019 with the company agreeing to pay $32.5 million.

Collecting Rocks

I’m not going to spend a lot of time on Gilbert’s other ventures, which include the Cavaliers and other sports teams, real estate, venture investments, casinos, and non-profits.

His bet on Detroit is worth noting because it speaks to his passion and business savvy. After realizing that promising young employees preferred working in cities to his suburban locations, he began to sketch out a move to Detroit in 2007. The first batch of 1,400 employees moved in 2010 and today the company is headquartered there. At a time when the city’s future looked bleak, Gilbert became a major investor in depressed real estate and was later one of the chairs of the Blight Removal Task Force.

"We started losing job candidates from universities like U-M and Michigan State. People would tell us, I love your company, but I want to go to Chicago or Boston or New York."

"It wasn't until my late 20s and early 30s, when I started traveling for business, to places like New York City and Los Angeles, that I realized how much we were missing. As I started visiting these great American cities, it hit me--man, how did we blow this so badly?"

This is a good overview of his more than $5 billion in investments in Detroit real estate which include both landmark buildings and new developments. Gilbert is also involved in a variety of companies with ties to the city.

"It's the opportunity to get in low and sell high. It's an untapped market from an intellectual standpoint, and from a physical standpoint there are great buildings. The idea is to get to the tipping point where companies start believing that they can't afford not to be in Detroit."

The NYT also profiled his vision in 2013.

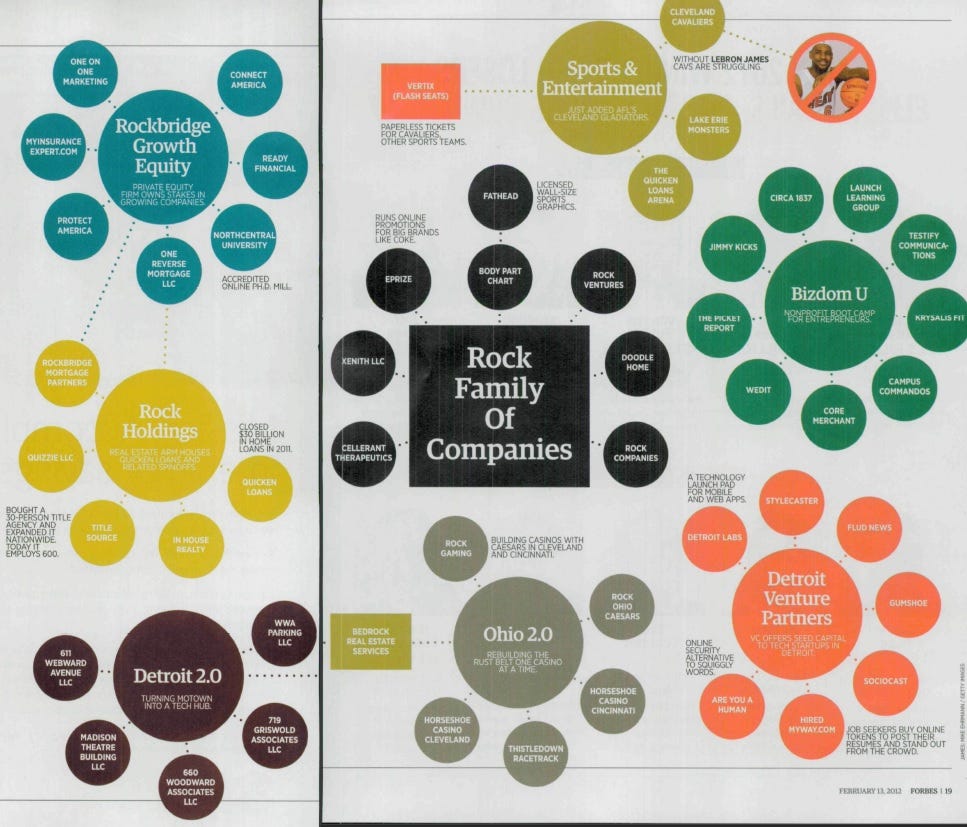

Gilbert’s web of companies, per Forbes:

Forbes, 2012

Quantifying Success

From Rocket Companies “Company Overview” (Form S-1)

“We are a Detroit-based company obsessed with helping our clients achieve the American dream of home ownership and financial freedom. We are committed to providing an industry-leading client experience powered by our award-winning culture and innovative technologies. We believe our widely recognized "Rocket" brand is synonymous with providing simple, fast, and trusted digital solutions for complex personal transactions.”

This captures all the key success factors that we’ve seen emerge in the company’s history. Quotes in this section are from the S-1.

Client Experience

“Our superior client experience is evidenced by our net promoter score (NPS) score of 74, a measure of consumer satisfaction, as compared to the average NPS of 16 for the mortgage origination industry according to J.D. Power.”

Speed of Closing

“A majority of our loans close within approximately 32 days from our receipt of client documents compared to approximately 43 days on average for the industry.”

Client Retention

The company built out its own servicing operation, again with metrics that indicate high customer satisfaction. This creates an opportunity to retain the borrowers upon refinancing.

“In 2019 we achieved overall client retention levels of 63%, and refinancing retention levels of 76%, which is approximately 3.5 times higher than the industry average of 22%. We have also been recognized with six consecutive J.D. Power awards for excellence in mortgage servicing, winning the award in each year we have been eligible to participate.”

Culture

We’ll talk about this in the next section.

Innovation

This includes both consumer-facing technology, such as the Rocket Mortgage app, and optimizing the back-end workflow.

“We are also more efficient due to our investment in technology and unique workflow processes. In 2019, we closed 6.7 loans per month per average production team member, compared to the industry average of 2.3 according to the Mortgage Bankers Association.”

Marketing

Not unlike a money center bank, the national scale of the direct-to-consumer model allows the company to invest heavily in its brand. In 2019, the company spent $900 million on marketing and advertising.

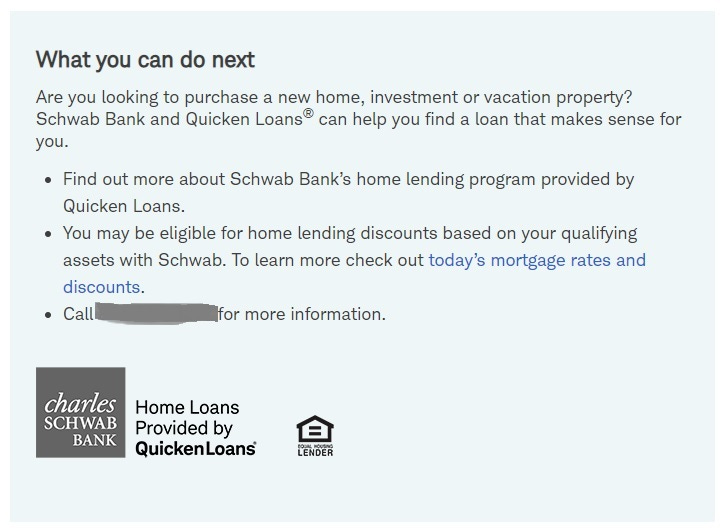

Following in Gilbert’s footsteps, the company has done creative marketing stunts like the Quicken Loans Billion Dollar Bracket with Warren Buffett. But it also invests in expensive high-profile ads such as at the Super Bowl. More recently, growth has been driven by building marketing partnerships with large financial companies such as American Express, Schwab, and, surprise, Intuit.

“Charles Schwab Bank – Home Loans Provided by QuickenLoans”

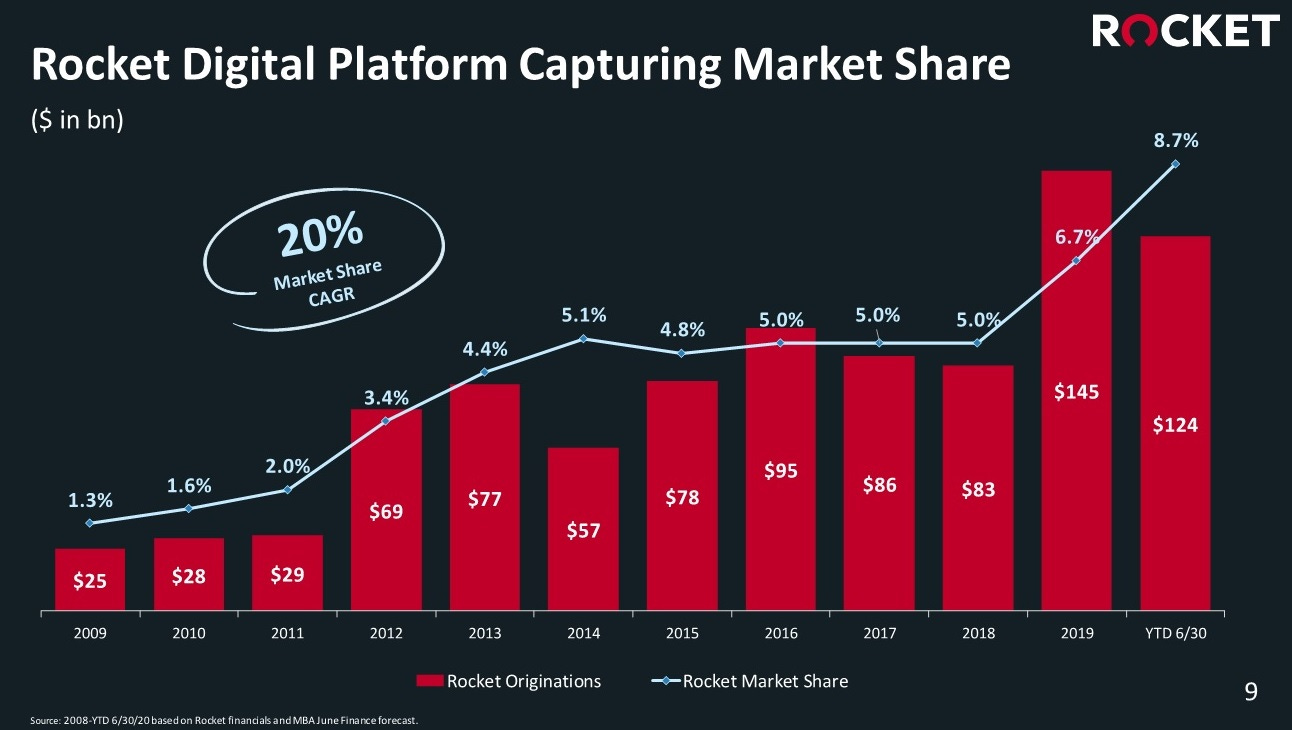

Direct to Consumer and Partner Network Originations Volume ($ in billions)

The longer-term question is whether it is possible to build a valuable brand for a commodity lending product like a residential mortgage. Can you position the Rocket Mortgage to stand for “mortgage online”? Or even “simple, fast, and trusted” for other personal financial transactions? Would borrowers be willing to pay a premium or would a strong brand just lower future customer acquisition cost?

As of right now, the heavy investment in marketing and partnerships with brand name partners have driven significant gains in market share.

Whether the company can sustain this edge will depend on continued execution and innovation – on the talent and culture at the company. Which brings us to:

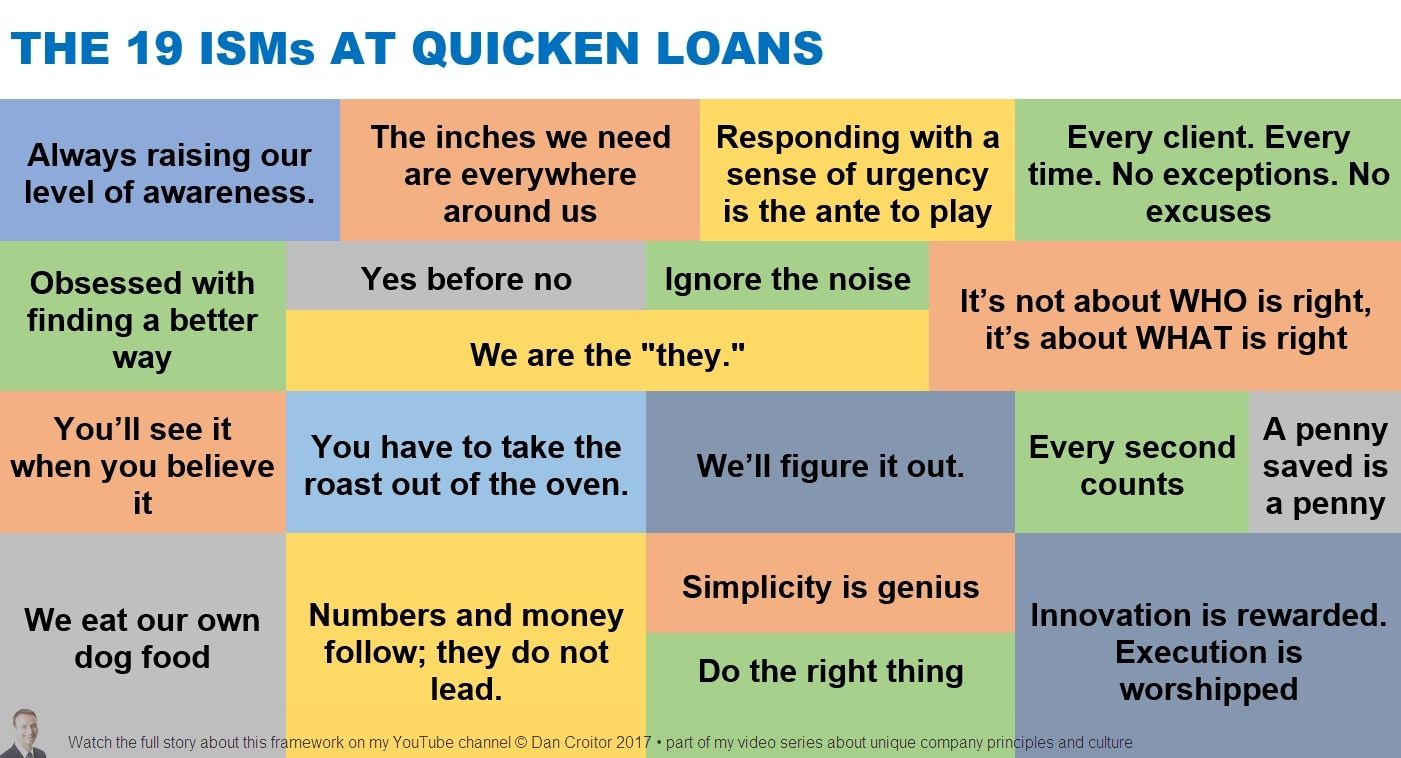

A Cultural Operating System: The 19 Isms

“It's who we are, which guides decision-making, your actions, your behaviors.”

“We probably prefer to hire people from outside of the mortgage business and train them in our way. We try to really get them involved in the culture of the company.”

From Rocket Companies “Company Overview” (Form S-1):

“Dan Gilbert, our founder and Chairman, purposefully created a strong cultural foundation of core principles, or "ISMs", as a cultural operating system to guide decision making by all of our team members.”

I really like this framing of a “cultural operating system.” The Isms are a collection of principles developed, or “discovered” as he says, by Gilbert over the course of 20 years. You can find them on their website. The company also regularly puts out a 144-page “Isms Book” with recent examples of the principles in action. It’s distributed to the employees at dozens of companies that are part of the broader Rock family. I have a pdf copy if you’re interested (email or DM for link).

The Isms cover a lot of ground, including action and execution, innovation and experimentation, responsibility, and resourcefulness. It’s a really compelling collection of ideas and will pick out a few that stood out to me.

"Core values, philosophy, culture... they drive every decision, action, behavior, and prioritization."

Focus on product, not accounting:

“Numbers and money follow, they do not lead.”

“Money and numbers are a measurement of actions. They don't have value in themselves. They are neither the ends nor the means. Chase the design, engineering and development of the product. Those who are motivated by building, improving and developing unique ideas and knowledge are the ones who acquire wealth.”

I don’t have much to add. A simple and powerful reminder to focus on building a great business, not a pretty sequence of quarterly earnings beats.

On focus and a sense of urgency:

“Every second counts.”

“Time, not money, is the most valuable commodity of all. Time can never be replaced. Never trade significant amounts of time for small sums of money.”

“A penny saved is a penny.”

“Choose to value your time. Invest it chasing pennies, and you will find pennies – and pennies never add up. Invest it in ideas, improving your skills, innovation, developing your talent, design, marketing, and technology, and your return will be more than just pennies.”

I like the essentialist sentiment here. Our time and attention are limited and valuable. Think carefully before committing to another goal.

On innovation, curiosity, and experimenting:

“Yes before no”

“Our bias is to the YES side of life. This is in stark contrast to the too common approach of an automatic NO to any expression of an inquiring mind. Saying NO is easier, but the status quo is not our favorite state. The only path to that place is through openness to the unknown.”

“Obsessed with finding a better way.”

“Finding a better way is not something we do on the side or when we get the time. Rather, it’s a key priority for every one of our team members.”

“We'll figure it out."““We don’t need to have all the answers before we take on a project or launch a new and innovative idea. We have faith that when it comes to some of the details, we’ll figure it out along the way.” “We know that building something new or creating something special is messy, and that greatness doesn’t always come in nice, tidy packages.”

“You have to take the roast out of the oven.”

“Perfection is not the goal when it’s time to make a decision. Focus instead on constant improvement and innovation. Over-analyzing can kill an idea and make you miss an opportunity. Don’t fear failure.”

I like that this goes beyond generic statements that “innovation is important.” Instead, it emphasizes the creation of conditions, of an environment that allows for innovation. By acknowledging that new ideas are risky and naturally face resistance and inertia. Also by removing any notion that new ideas have to be perfected before being tried out.

“If you try to be perfect before you make a decision or roll something out, in today's world you're going to get killed. You can't be perfect and it's better to clean up a little bit than try to be perfect and delay six months, a year, two years, and some competitor steals your thunder. Perfectionism does not marry entrepreneurialism in a good way. Something has to give and I prefer that the perfectionist side gives.”

As Michael Bloomberg said:

“My main job is to keep us from developing a structure that will preclude a kid we just hired from walking through the door and saying 'Why not try this.'"

Or Jeff Bezos:

“One of my jobs as the leader of Amazon is to encourage people to be bold. It’s incredibly hard to get people to take bold bets. And you need to encourage that. Experiments are, by their very nature, prone to failure but big successes – a few big successes compensate for dozens and dozens of things that didn’t work.”

On customer service:

"Every client. Every time. No exceptions. No excuses."

Gilbert was once told that two prospects had complained that Quicken had not returned their phone calls. He wrote another one of his company-wide emails, in all capital letters: "WE RETURN PHONE CALLS TO EVERYONE EVERY TIME."

"Clients don't care how much you know until they know how much you care."

And finally, what other company quotes Al Pacino in its principles?

"The inches we need are everywhere around us."

“You find out life’s this game of inches. So is football. Because in either game, life or football, the margin for error is so small -- I mean one-half a step too late, or too early, and you don’t quite make it. One-half second too slow, too fast, you don’t quite catch it. The inches we need are everywhere around us. They’re in every break of the game, every minute, every second. On this team, we fight for that inch. Because we know when we add up all those inches that’s gonna make the fuckin' difference between winning and losing.”

And the Rock/Gilbert version:

“But, if a company does thousands of little things better than anyone else, they become nearly impossible to imitate. We call those thousands of little things “inches.” We’d never be able to foresee all the things that should be noticed or improved. Instead, we drive a culture that motivates our team members to find the inches we need all around us. We are all empowered to find the opportunities to make an impact everywhere; one inch at a time, these inches all add up to greatness.”

This one has it all: competitive spirit, resourcefulness, resilience, and teamwork. More importantly, it emphasizes process over outcome. Remember that all the small decisions add up, all the times when you push harder and stretch further.

Wrapping Up

With the benefit of hindsight, the story of Rocket Companies looks straightforward. It’s as if Gilbert and his team always had a sense of what was coming around the corner and made the right call. Not only did the company aggressively move online, it was obsessed with customer experience and shrinking the gap between intent and delivery.

But as CEO Jay Farner wrote in the prospectus, “building something great is messy.” And I’m sure it was, not just when the mortgage crisis hit. As Charlie Songhurst recently pointed out on Invest Like the Best, “managerial diseconomies of scale” can be a tremendous obstacle when scaling up a company. And Rocket Companies has scaled to 20,000 employees.

"We're in the people, recruiting, and talent business. It's all about people. You can't spend enough time finding, recruiting, and developing your leaders."

"If you're gonna be an excellent company, who you have on your team is going to be the difference."

In “Good to Great” Jim Collins called it putting the “who” before the “what.” The importance of first assembling a world class team who can then tackle challenges, rather than coming up with the strategy first, followed by hiring talent. From everything I’ve seen, Dan Gilbert and his team have had remarkable success by focusing on culture and talent, fostering innovation and execution. It’s a winning formula in any boring industry.

“Innovation is rewarded. Execution is worshipped.”

If you enjoyed this post, please sign up and share it with your friends. Thank you so much!