Zooming in on history

Zooming in on history

Indulgent repetition, rapture ideology, and scale models of HumanOS

If you enjoy exploring the business of life and investing, join 3,816 subscribers for free weekly content.

“Nowhere does history indulge in repetitions so often or so uniformly as in Wall Street. When you read contemporary accounts of booms or panics the one thing that strikes you most forcibly is how little either stock speculation or stock speculators to-day differ from yesterday. The game does not change and neither does human nature.” -Edwin Lefèvre, Reminiscences of a Stock Operator

I used to think that history provided the right framework for investing. I saw markets as a never-ending dance of cycles in which the sober-minded benefited from the crowd’s occasional madness. It is easy to adopt this mindset if you start your journey reading about value investors whose careers are often defined by moments in which they refuse to participate in the party (only to load up on bargains later). But history alone is a treacherous guide.

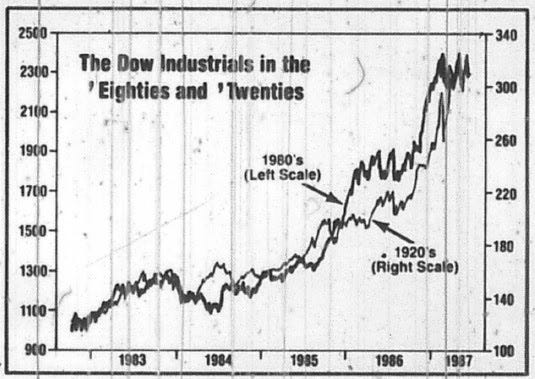

When I recently wrote about Julian Robertson’s test of conviction during the crash of 1987, I tried to find a spectrum of bullish and bearish post-crash takes. I found bears: Paul Tudor Jones, Marty Zweig, Jim Rogers, Felix Zulauf. And bulls: Julian Robertson, Peter Lynch, Mario Gabelli, Ron Baron, John Neff, Robert Wilson. At least in this small sample, it seemed to boil down to macro vs. micro. Those who took a historical perspective seemed to view price as a signal – they interpreted the crash as the opening salvo in a downcycle in which the market would lead fundamentals. They saw parallels to the 1920s, another decade of excess and skyrocketing debt levels.

Stanley Druckenmiller explicitly talked about this reflexivity when he warned: "I'm categorically against anyone making any further downward predictions. They could become self-fulfilling, and help send the economy downward. We're all Americans and none of us wants the economy to fall apart whether we're short or long."

But the bottom-up bulls turned out to be right. Price was not a signal, and the stock market didn’t lead the economy. Instead, lower rates and a lower dollar helped ailing industrial companies and the market started to recover.

Contrarians armed with a big historical analogy risk falling into a kind of “rapture ideology.” The state of the world looks broken, corrupted by excess, and headed for a reckoning. The true believers, who own the right asset, will be saved. The rest? NGMI. (Not going to make it.) In other words: it's divine punishment for those who made money “the wrong way.” And salvation for the chosen few who resisted temptation and remained on the righteous path.

Some examples that come to mind are crash prophets (a market collapse awaits the speculators), value and distress investors with big cash balances (the cleansing brushfire of recession shall reward them with deep value bargains), as well as gold bugs and Bitcoin maximalists (only sheep hold their money in fiat).

But history doesn’t just offer doom and gloom — it can also lull us into false comfort when key conditions change. I’m working on a detailed piece about Bill Miller and every time I mention his name someone helpfully points out that he was crushed in 2008. While there were several reasons for this, I suspect that one of them was that he started reasoning by analogy. In 2007, he wrote about “the worst housing market since the early 1990’s. Had you bought housing stocks during that previous period of duress, you would have made many times your money and handily outperformed the market over the subsequent decade.” But 2008 was different.

A friend recently joked that knowledge of history has probably been inversely correlated with investment success over the past decade (the rapture ideologue inside me immediately interpreted this as a sure sign of an impending market top). Should we abandon history and focus all of our attention on the present and studying change? I asked Jim O’Shaughnessy, one of my favorite finance history enthusiasts, for his take: “the mistake (I think) many people make is extrapolating from the EVENT rather than the way our HumanOS pretty much guarantees we will react to it. So, I would argue that it is far more important to understand human nature and the relatively systematic way it kicks in around various events than actual historical events.” Instead, Jim likes to point out that “arbitraging human nature,” is the “final edge.”

The difficulty, of course, is that we are all running said Human Operating System and are just as likely to make mistakes that can be exploited by others. As Bill Miller pointed out: “One of the enduring features of the findings in behavioral psychology as it applies to finance is the almost complete inability of those who are aware of them to actually apply them. You can attend Richard Zeckhauser’s seminars at Harvard, read lots of articles and case studies, be reminded of how recency bias, or anchoring, or the representative fallacy, or myopic loss aversion impair clear thinking and skew decision making, and still fall prey to them and others of their ilk the moment you are confronted with real world situations.”

No wonder O’Shaughnessy chose to be a quant.

Scale models

I recently started reading George Saunders' A Swim in a Pond in the Rain, basically a written version of his class on Russian short stories (and a fascinating book so far). Saunders wrote about “perhaps the most radical idea of all,” namely that “every human being is worthy of attention and that the origins of every good and evil capability of the universe may be found by observing a single, even very humble, person and the turnings of his or her mind.”

In other words: we zoom in all the way on one moment in one person’s life to look for a greater truth. Saunders called this a scale model of the world. For a dozen or so pages we step into another person’s shoes and experience their version of the human condition. It reminded me of reading biographies which are another way of learning about the past. Marc Andressen said:

“There are thousands of years of history in which lots and lots of very smart people worked very hard and ran all kinds of experiments on inventing new technologies, or creating new businesses, or new ways to manage or new ways to lead or all kinds of things. At some point, somebody put them down in a book, and for very little money and for a few hours of time, you can literally learn from somebody's accumulated experience. And I think there's just, there is so much more to learn from the past than I think that we often realize.”

Following the framework in From Predators to Icons, I think of business biographies as starting with a set of conditions which enable a crucial decision with which the protagonist begins their journey and leaves the “ordinary” world (the world of ordinary results, if you will). While there are infinite paths to wealth, the basic pattern is not complex (I think). It starts with a cash flow stream (a product, new technology, business, real estate, you name it). Someone either creates the asset or acquires ownership. They typically apply elements of leverage to magnify the outcome (labor, capital, technology). And there is a timing component: can the process compound through organic growth, reinvestment, or new investment and acquisition opportunities.

And yet, understanding the conditions and decisions that lead to success is not enough. Saunders steps through the Russian short stories page by page asking, “is it story yet” (sic). What he means is: has something happened yet that changed the character forever? Without change there is no story. We are just confronted with a lifeless sequence of events. I try to ask the same question when reading a biography. For example, I find it hard to relate to, and learn from, an escalating series of wins: “founder has an idea, writes amazing code, is showered with VC money, successful IPO, the end.” Yawn. This is one reason why I was drawn to Miller’s story. Mistakes and adversity challenge us to change.

I still enjoy learning about the drama of financial history and find it very entertaining. However, I have become more cautious about using it as a guide. Instead, I try to pay more attention to the conditions and how they have changed. And I remain confident that there is much to learn from the interesting and successful people who walked the path before us. Their lives can teach us about the human condition and about navigating human systems: markets, institutions, and networks. While the specific lessons about achieving success can lose their relevance, lessons about the HumanOS are timeless.

“We’re going to enter seven fastidiously constructed scale models of the world, made for a specific purpose that our time maybe doesn’t fully endorse but that these writers accepted implicitly as the aim of art—namely, to ask the big questions, questions like, How are we supposed to be living down here? What were we put here to accomplish? What should we value? What is truth, anyway, and how might we recognize it? How can we feel any peace when some people have everything and others have nothing? How are we supposed to live with joy in a world that seems to want us to love other people but then roughly separates us from them in the end, no matter what?” George Saunders, A Swim in a Pond in the Rain

Enjoyed this piece? Let me know by hitting the ❤ like button.👇 Thank you!😉